Economic Perspective and Housing Marketing Dynamics

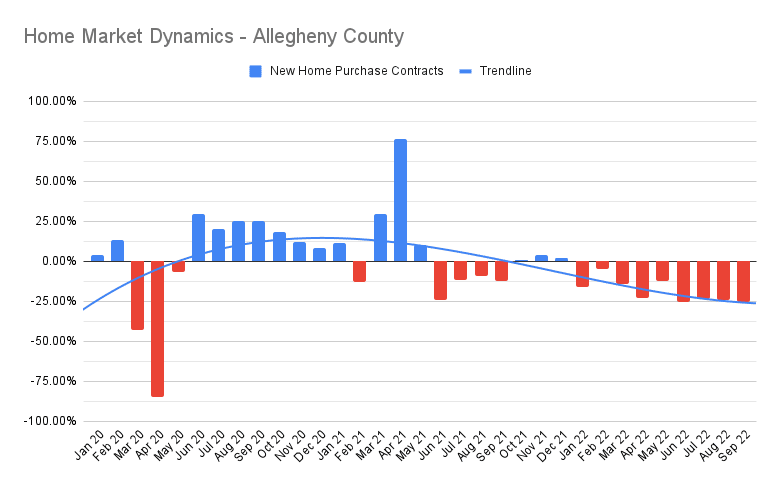

Allegheny County has recovered from most of the job losses due to COVID-19. In March of 2020 the U.S saw a record 6 week job loss of 22 Million. This stunted many of the Year over Year statistics, given that the market was essentially paused during spring of 2020, which was shaping up to be another record year. Increases across the board for the number of houses sold, and other valuation statistics then appear to shoot through the roof for 2021 with all of the catch up buyer demand and reporting. Therefore when you are comparing homes sold in Spring of 2022 to Spring of 2021, it’s like comparing 2022 to two years worth of sales. Not to sugar coat that on top of that, things have appeared to slow down, but not as bad as most numbers would make it seem.

Our economy is being faced with historically high inflation, due to that inflation, lender’s need to charge more to ensure they will make a profit. If the bank lends to a customer at 5%, but inflation is 6%, the bank is going to be losing money, so they need to raise their rates to ensure they are taking inflation into consideration. Additionally, inflation is now outpacing wage growth. This puts a ceiling on home prices because home prices can only grow so fast through inflation before banks are no longer able to underwrite the buyer for the loan. According to the Federal Reserve, revolving credit card debt and delinquency payments have increased a seasonally adjusted 6.8% in the 3rd quarter of this year.

Economic growth is collapsing as a recession draws near. According to the Bureau of Economic Analysis our GDP has hovered around -1% the majority of this year. The government looks to control inflation through the Federal Reserve. It would appear after ignoring inflation, or hoping it would go away on its own that the market would stabilize itself. When that did not come to realization, the Government then began to slowly ratchet up interest rates from the federal reserve. With inflation still out of control, the Government feels they have no other choice but to induce a controlled recession.

The Federal Reserve has 3 main ways of influencing the economy. The first way, and most obvious, is their ability to raise and lower interest rates. By setting the prime rate at which major banks are able to borrow money from the federal reserve. The second way is by purchasing assets on the open public market, for example purchasing a company that might be going under, they are able to inject cash into the business in exchange for shares, which they can then sell back after the economy recovers. The third way is through monetary policy, in which they can pass regulations on acceptable lending practices, and how much a bank must be required to hold in reserve.

Seller’s can expect to be taking the reduction of the increased amount a borrower will need to pay to purchase the home off of their sales price. Buyer’s can expect to see more selection of homes on the market and also receive more opportunity to negotiate through the terms of the sale.

Our prediction is that any recession will be short lived and low in the amount of asset value loss. As the economy slows and unemployment rises, the Government will most likely begin to reduce interest rates again, which will allow the wheels of the economy to begin to turn again. In the meantime, sellers are still able to sell at near historic peak values, and buyers still have the opportunity to purchase a home they love and refinance it later down the line when rates drop, facing less purchasing competition and gaining more leverage in the meantime.